Trading Is Not A Dirty Word

“….no senior managers actually wanted to get their hands dirty and investigate the numbers.…….. they never dared ask me any basic questions, since they were afraid of looking stupid about not understanding futures and options.” – Nick Leeson, Rogue Trader

Since the beginning of 2025 Consilience has published two blogs:

- The first, “Oil Prices: When Does Complex become Too Complicated”, described how oil prices are agreed, focusing on the oil price negotiation that takes place when oil cargoes change hands. It explained that, when the composition of a published oil price benchmark changes, the price differential to the benchmark in contracts for non-benchmark oil has to be reviewed;

- The second, “Spoiled for Choice”, explored the value of options, or choices, given to an oil major or large trading company by a non-trading exploration and production (“E&P”) company or small refiner/consumer without its own trading capability. It considered how much such optionality in the contract price formula is worth from the perspective of the non-trading option grantor.

This third blog will look at the value of oil price optionality in a non-benchmark contract price formula from the perspective of the larger oil or trading company. It might be expected that, if the smaller non-trading company understands how much its trading counterparty is making, that should go some way to wresting a bigger share of the economic rent accruing to the trader from the option- right? Alas, it is not that simple.

As we said in “Spoiled for Choice”, “It should be understood that as between the two counterparties to the physical sale and purchase agreement, the size of the option premium is a zero-sum game. However, the more active trading company is unlikely to be just buying the option to set the B/L date and the price averaging period and leaving it at that. It is likely that the cargo in question will form just one component of an arbitrage jigsaw puzzle, which will involve, in all probability, a number of financial and operational risks that must be hedged.” arbitrage jigsaw puzzle, which will involve, in all probability, a number of financial and operational risks that must be hedged.”

The Long and the Short of it

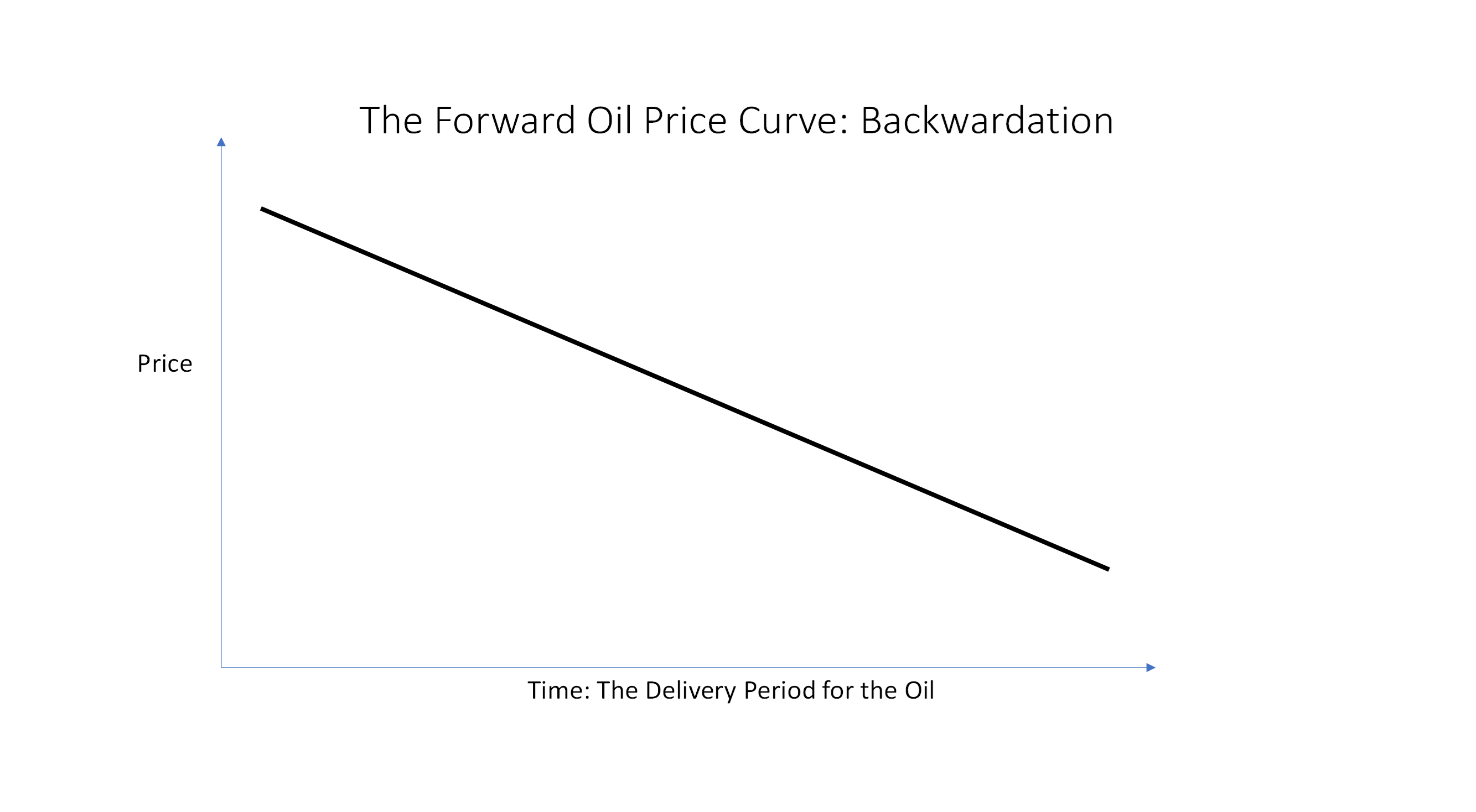

There is a widely held view that traders are gamblers who make their money from outguessing the next move in market prices. This may be a move in the height of the forward oil price curve (“A”), or the slope of the price curve, (“T”), as explained in our previous blogs.

It is believed by some that traders buy, i.e., go “long”, of a commodity or asset and wait for the price to rise so that they can sell it for a profit. In other words, buy low, sell high. Or they may go “short”, i.e., sell a commodity or asset for forward delivery that they have not yet acquired in expectation of falling prices. They expect to cover their short position by buying in before they have to deliver the physical commodity. In other words, sell high, buy low.

This form of speculative activity is just one arrow in the quiver of a trading company, but not necessarily the sharpest, or most regularly used, one. It is capital intensive and very risky, particularly in a geopolitical and volatile commodity like oil. It is written on the gravestones of various speculative trading companies: “We bought high and sold low. Doh!”

Trading businesses are more likely to rely on arbitrage opportunities for their bread and butter, rather than naked speculation.

Arbitrage

Arbitrage is the act of profiting by discrepancies in prices due to, for example,

- imperfect knowledge;

- location;

- illiquidity;

- seasonality;

- different product specifications in different regions;

- different environmental regulation in different regions;

- slow communication of new information; or,

- any other reason, such as the inability of two counterparties to deal with each other directly and therefore needing to insert a “sleeve” company into the chain of supply.

Usually, price imperfections are small and transient, because traders quickly recognise and exploit any such inconsistencies. Traders will sell those prices, or price components, that are over-valued, driving the price down, and buy those price components that are undervalued, driving the price up, so that they rapidly come back into an economically consistent line.

Examples of Arbitrage

Location: If the price of a product is different between two locations in the world, the trader may buy in the cheaper location and sell in the more expensive location. This activity continues until the cost of freight and the time value of money make it uneconomic.

Timing: If the price of oil for delivery in the near future is less than the price of oil for delivery in a later period (contango), the trader may buy oil and take delivery now and sell it for delivery later. This activity continues until the cost of storage and the time value of money make it uneconomic.

Quality: If the price of one specification of a product is lower than the price of a different specification of the same or a similar product, the trader may buy the cheaper oil and blend it to the specification of the more expensive product. This activity continues until the cost of blending components, freight, storage and the time value of money make it uneconomic.

Arbitrage is not risk free. The purchase and sales prices or price formulae have to be hedged. Otherwise, the arbitrage gain can be lost in a movement in the absolute price, A, or the time differential, T. This can be trickier in the case of a quality arbitrage because of the seasonal changes in product demand and specifications, and the blunter hedging tools available in the refined products market than in the crude oil market.

Illustrative Example

Readers whose day job is not trading may find it unnecessary to slog through the following example. We at Consilience have often found it helpful to work through some examples like this with industrial company board members, audit committees, regulators and judges/arbitrators in disputes to demystify the trading game. The explanation below is somewhat detailed and turgid, but it is not intellectually challenging. Those with a more superficial interest may wish to skip forward to the heading “Shooting at a Moving Target: Bullets are Costly”.

Using an old copy of Platts from 13th February 2024, (See extracts below) here's how it might work in one scenario:

On 13th February 2024, a third-party oil seller, which we will call (“Explorer”), agrees to sell a cargo to a trader, which we will call (“Trader”) for delivery in four weeks’ time. Four weeks forward from 13th February is the working week of 4-8th March 2024. The parties may agree to deem the bill of lading (“B/L”) date in advance as, say, 6th March. We discussed deeming in our previous blog.

To illustrate the issues, we will assume that the physical oil contract price formula that has been agreed is, say, the 2-1-2 average of Platts Dated Brent published on the 5 days around the B/L date +/- a grade differential, which we are calling “G”, as in previous blogs. G accounts for any differences between the Platts assessment parameters of Dated Brent and the characteristics of the physical oil in question.

The price component, G, is not easily hedgeable and is the most rigorously negotiated component of the price formula. It is where the Trader hopes to capture a profit. But in pursuing this profit, the Trader must ensure that any gain it makes on G is not lost in movements in the the slope of that curve, T, between 13th February when it buys the cargo from the Explorer and some later date when it sells the cargo to an as yet unknown third party on as yet unknown terms or in the height of the forward oil price curve, A, after 4-8th March. The components A and T were described in the previous blog.

The Trader’s price exposure must now be hedged.

EXTRACT ONE

Source: Platts

Extract one shows, among other things, Platts current assessment on 13th February of Dated Brent for delivery 10-30 days forward from 13th February, and the simultaneous assessment of forward cash Brent for delivery in M1, which is April, M2, which is May and M3, which is June.

The report shows a “bid-offer spread”, i.e., the price bid by the best buyer and the price offered by the best seller, at market on close when the PRAs make their assessments. It also shows the midpoint of that bid-offer range as an assessment of the likely price that would be agreed if a deal was actually to be transacted.

As we pointed out in our first blog “Often it is not actual deals negotiated and finalised in a contract that form the benchmark database for each grade of oil. It is frequently just price indications to buy or sell that do not result in an actual deal. And those deals and indications are those submitted to a price reporting agency (“PRA”) during a specific 15-minute period on an electronic platform each day. Only those companies that have been pre-approved by the PRA are permitted to input price indications to the PRA’s electronic platform. “

Extract Two shows Platts’ assessments of CFDs up to 8 weeks forward expressed as the Dated Brent differential to its own M2 Brent cash contract quotation. In reality, the CFD market trades up to 12 weeks forward expressed as a Dated Brent differential to M1, M2 or M3 as the two counterparties to any deal might agree.

EXTRACT TWO

Source: Platts

As mentioned above, although the PRAs publish CFD assessments up to 8 weeks forward from the publication date, the market trades up to 12 weeks forward, albeit in progressively lower volumes. Brokers can be consulted to obtain quotes for these further forward weeks, but a rough, back of the envelope assessment can be obtained by extrapolating the difference between CFD Week 7 and CFD Week 8. So, for example, CFD Week 9, namely 8-12th April, on 13th February may be estimated as May cash Brent minus $0.30/bbl, i.e., (($0.06-0.12)-0.12)) =-$0.30/bbl.

CFD Weeks 1 to 12 are separate contracts.These refer to the current value on 13th February of the average difference between Dated Brent and the month 2, M2, forward cash Brent contract,which is to be published in each day of delivery Week 1, 12th-16th February, delivery Week 2, 19th-23rd February etc. These are expressed as a price premium or discount to the M2 cash Brent contract for the delivery week in question.

Some care must be taken when trading CFDs, particularly in the later weeks. This is because if, say, a Week 9 CFD is expressed as a differential to the May M2 Brent cash contract when it is purchased on 13th February, it will cash settle by reference to the Dated Brent minus May Brent differential as published by the PRA during Week 9, i.e., 8-12th April. However, by the time a Week 9 CFD comes to cash settle, the May cash contract will no longer be assessed by the PRAs and the May futures contract will have expired. So, a hedge of a late week CFD on 13th February may have to be managed by rolling the May component forward to June at some point before the physical sales price averages out. We will show how this may be done later in this narrative.

Published price data, futures contracts and broker quotations allow us to construct a detailed forward oil price curve showing the value of oil for delivery on very precise future time periods. Chart One shows the forward oil price curve suggested by Platts data on 13th February. The curve is showing pronounced backwardation, as discussed in our last blog.

Chart One: The Forward Oil Price Curve on 13th February 2024.

Source: Derived from Platts Extracts One and Two above

In our illustrative example of a sale and purchase contract for oil for delivery on a deemed B/L date of 6th March, with the price averaging period being the 5 days around the deemed B/L date, i.e., 2-1-2 pricing, the value of the contract on 13th February according to Platts assessments is:

- May cash Brent $82.42/bbl; plus,

- CFD Week 4, $1.37/bbl; plus/minus,

- G.

This is equivalent to $83.79 +/- G/bbl. This information is transient and is only useful if the Trader acts upon it. The actual contract price on the invoice that the Explorer sends to the Trader in due course will be based on actual published prices averaged over 4-8th March.

So, on 13th February, the Traderis now long of, i.e., committed to buy, a physical cargo for delivery on a deemed B/L of 6th March based on Dated Brent averaged over the 4-8th March, as published by Platts, +/- G. The Trader may only have got itself into this position because it could identify an arbitrage opportunity, or in its judgement the likelihood of an arbitrage opportunity, to make a profit on the value of G by using one of the arbitrage strategies identified above. For clarity we will label the value of G in the Trader’s purchase contract from the Explorer as G1.

Armed with this explanation of the data available, for illustrative purposes we will assume a locational arbitrage where the cargo may be delivered in a later period to a different location where the value of G is sufficiently higher to cover the negative impact of backwardation, the cost of freight and the time value of money. We will label the value of G in the Trader ‘s onward sales contract to a refiner as G2.

So, on or after 13th February, the Trader may sell the cargo perhaps to a refining company, which we will dub (“Refiner”). This may be a contract for delivery, say, 1st -3rd April, with a deemed discharge date of, perhaps, 2nd April with Dated Brent pricing averaged over 5 days after the deemed discharge date. That would be the Platts publication dates of 3-9th April 2024.

Already this is looking like a tricky deal.The market is in backwardation so, since the act of transporting the oil to a different geographic region takes time, the current market for later- delivered oil is already significantly below oil for delivery nearer term. Based on the values of A+T for 4-8th March 2024 and for 3rd-9th April 2024 alone, this is a loss-making deal. So, to proceed, the Trader must have a reasonable expectation that the value of G2 will be greater than G1 by at least the extent of backwardation and must also compensate for the cost of freight and the time value of money.

While the Trader is focusing on arbitraging the value of G, elsewhere the height, A, and the slope, T, of the oil price curve are in constant motion and do not maintain the values that the Trader identified when it decided to proceed with the arbitrage on 13th February. If the height of the curve, A, falls and/or the slope of the curve, T, rises between 4-8th March, when the Trader’s purchase price averages out and by 3-9th April, when the Trader’s sales price averages out, the Trader’s anticipated profit, G2 minus G1, may be diminished or eliminated.

If the Trader judges that the arbitrage was worthwhile on 13th February, it would make sense to lock in the value of T that was apparent on 13th February, and the value of A that emerges 4-8th March, lest they move against the arbitrage profit. There are various ways that both A and T maybe hedged if the Trader does not intend to speculate on their values in this, its long physical position.

Hedging

The Trader is at risk if the purchase price of Dated Brent 4-8th March +G1 turns out to be higher than the sales price of Dated Brent 3-9th April +G2 + cost of freight + the time value of money. On 13th February Trader is probably making money on this deal on a mark-to-market basis, or it would not do the deal. Or the Trader may consider that it is worth taking a speculative risk even if a profit is not obvious on 13th February because it may judge that the market will move in its favour.

But we will assume for illustrative purposes that the Trader identifies a profit on 13th February and wishes to lock in that profit. It must now, on 13th February, hedge the values of the difference between CFD Week 4-8th March and CFD Week 3-9th April. To do this it must:

- Hedge 1: Buy CFD Week 4, 4-8th March, at M2 cash Brent, May,plus $1.37/bbl;

- Hedge 2: Sell three fifths of CFD Week 8 and two fifths of CFD Week 9, 3-9th April, at M2 cash Brent, May, minus $0.19/bbl (i.e., 3/5 times -$0.12 plus 2/5 times -$0.30= - $0.19/bbl)

Hedge 1 will cash settle automatically by the Trader, in effect, selling back the average Dated Brent v May Brent differential as published by the PRA over 4-8th March. It is mostly irrelevant to the Trader’s overall arbitrage profit what the value of the Dated Brent average turns out to be: it may be higher or lower than the fixed value at which the CFD was purchased on 13th February, i.e., May Brent plus $1.37/bbl. This is because the hedge sale cash settlement price will mirror and cancel out the Dated Brent component of the physical cash purchase price between the Explorer and the Trader.

Hedge 2 would cash settle automatically by the Trader, in effect, buying back the average Dated Brent v May Brent differential as published by the PRA over 3-9th April. However, there is a catch attributable to the May contract expiry date. This will be explained in the next section of this blog. It is again mostly irrelevant to the Trader’s overall arbitrage profit what the value of the Dated Brent v forward cash Brent average actually turns out to be: it may be higher or lower than the fixed value at which the CFD was sold on 13th February, i.e., May Brent minus $0.19/bbl. This is because the hedge purchase cash settlement price will mirror and cancel out the Dated Brent component of the physical cash sales price between the Trader and the Refiner.

It is likely that the Trader will choose the futures contract as its hedging tool, rather than the 30-Day BFOETM forward cash contract. The cash contract trades in cargo volumes for 700,000 bbls at at time, not 20% of an unspecified physical cargo volume. The futures contract trades at fixed volumes of 1,000 bbls at a time and is much more useful for precision hedging. The value of T, the slope of the curve, may be hedged using the Dated to Frontline (“DFL”) contract, the equivalent of the CFD contract but based on the differential between Dated Brent and the first futures contract, rather than Dated Brent and the M2 cash forward contract.

Roll Out the BBLs

As indicated above, the May Brent component of both these CFD hedges opens up a further risk: if the height of the forward oil price curve, A, as expressed by the price of May M2 cash Brent, falls between 4-8th March and 3-9th April, the Trader’s arbitrage outcome will be less than it expected on 13th February when it was set up.

To protect itself from a fall in the height of the forward oil price curve, A, the Trader may sell the May futures contract over the five publication dates of 4-8 March, to cancel out the absolute price exposure, A, on its purchase contract from the Explorer. It will intend to buy back the May futures contract over the five publication dates of 3-9th April, to cancel out the absolute price exposure, A, on its sales contract to the Refiner.

However, the Trader cannot buy back a May futures contract 3-9th April, because the May contract will have expired at the end of March. So, at sometime before the end of March, the Trader will have to close its short May futures position by buying the cargo volume on or before the May contract expires and reopen a new short position in the following futures contract month of June.

- Hedge 3: Sell, i.e. go short, May futures over the 5 days of 4-8th March, 20% of the cargo volume per day;

- Hedge 4: Buy back May futures on or before end March, 100% of the cargo volume;

- Hedge 5: Sell, i.e. go short, June futures on or before end March, 100% of the cargo volume;

- Hedge 6: Buy back June futures 3-9th April, 20% of the cargo volume per day.

Now the Trader can buy back its short June futures position over the five publication dates of 3-9ᵗʰ April, to cancel out the absolute price exposure, A, on its sales contract to the Refiner.

Alternatively, on 13th February, the Trader may have anticipated the need to close its hedge over 3-9th April. Being well aware of the expiry date of the May futures contract, the Trader may on 13th February have entered into its CFD Hedges 1 and 2 above based on the published price differential between Dated Brent and M3 cash Brent, June, rather than M2 cash Brent, May. The PRAs choose to publish CFD assessments based on the published price differential between Dated Brent and M2 cash Brent. But two counterparties may construct a CFD trade with whatever structure they both agree, including based on the published price differential between Dated Brent and M3 cash Brent.

In either case, the Trader is exposed inevitably to the May/June cash Brent price spread either on 13th February, or on any of the dates between 13th February and the expiry of the May futures contract that it chooses to roll forward its hedge of the absolute oil price, A.

It is mostly irrelevant to the Trader’s overall arbitrage profit what the outcome of its futures Brent contract purchases and sales turns out to be: it may make a profit or a loss on these hedges. If it makes a profit, it will be because the height of the forward oil price curve has fallen, and it is buying back its futures hedges at a lower price. But this gain will be offset by the loss it makes between its physical purchase from the Explorer and its sale to the Refiner.

Shooting at a Moving Target: Bullets are Costly

The preceding discussion describes one possible scenario where the Trader identifies an arbitrage opportunity on 13th February that relies on its ability to agree a value of G2 that exceeds G1 by enough to cover backwardation and its other costs. That is unlikely to be the end of the story for the Trader.

During all the time period from 13th February, when the purchase contract from the Explorer is agreed, up until 1-3rd April, when the cargo is delivered to the Refiner, the Trader will be on the look out to improve its profit estimate, G2-G1. Perhaps this might be by substituting a different cargo for delivery to the Refiner and delivering the Explorer’s cargo to a different location, perhaps co-loading with oil from a different source to improve its freight economics or blending a product in-tanker to meet different regional quality specifications.

Each time the Trader changes its arbitrage strategy it has to undo its hedges that were appropriate for the first strategy and put new ones in place to suit its new strategy. This activity is not cost free. The Trader must cope with a bid-offer spread at the time of dealing, sometimes tying up its credit lines with swap providers, paying brokerage fees and the depositing initial margin and variation margin with a futures exchange. These margins are security deposits paid to the exchange’s clearing house to guarantee payment and performance.

If the Trader hedges its absolute price risk, A, using the futures contract, rather than the forward cash Brent contract applicable to the physical cargo, it will also suffer basis risk attributable to the fact that the futures and the forward contract do not trade at exactly identical prices. The difference is referred to as the Exchange for Physical (“EFP”) difference and can be up to 10 cents/bbl, but more often around 5 cents/bbl.

Furthermore, the Trader is using a fixed volume financial instrument, CFDs, DFLs or futures, to hedge a variable volume physical contract. Most physical seaborne cargoes have an operational tolerance of +/- 5-10%, which was originally established to give the Master of the tanker flexibility to adjust the trim of the vessel or to sail light-loaded for safety reasons. So, if the physical cargo volume varies from the base contract volume the Trader may be over-hedged or under-hedged.

This also presents an opportunity. This operational tolerance is often appropriated by the Trader who has chartered the tanker for commercial reasons. If the Trader is making money on the hedge side of its profit/loss equation and therefore must be losing money on the physical cargo size of the equation, it can choose to load 5-10% less on the tanker carrying the physical cargo to boost its overall profit.

Herding Cats

Large oil companies and trading companies are likely to have many different deals in progress, often traded in different offices around the world. All of these deals may need to be hedged and re-hedged to reduce speculative risk. To defray their dealing costs, such companies will often centralise their risk management activity, as illustrated below.

So, instead of each individual trader or trading desk within a trading company entering the market each time it has a risk to hedge, each such trader will undertake its hedge with the company’s own Central Risk Management desk (“CRMD”), marking the hedge to market at the time each trader logs a deal with CRMD. That mark to market value is the hedge price recorded on the individual trader’s profit and loss account for the cargo it is hedging. What the CRMD does with the risk transferred to it by the individual trader is up to the risk manager.

This is one of the reasons it is so difficult, but not impossible, to bring hedge gains and losses into the calculation when assessing damages in a trading dispute. It requires extremely detailed enquiry into the trade capture software of the hedging company. It also requires drawing a ring fence around the P&L account of the trader entering into hedges with its own CRMD.

To manage overall corporate price risk the CRMD may look for internal offsets in-house before laying off the Trader’s risk in the market or deciding to transfer it to a central corporate speculative trading book.

Trading is a capital-intensive activity, not often appropriate to the business models of companies like the Explorer and the Refiner. It is not a slam dunk opportunity for traders to print money.

Price Optionality

In the light of the foregoing brief and simplified example of how a trader might go about generating a profit, we can now turn to the main purpose of this blog. This is to assess how much a small producer or refining/consuming company should charge a large oil or trading company for the option to deem the B/L date or choose the price averaging period in a sale and purchase contract.

Looking back at Platts Extract Two above, it is immediately apparent that, on 13th February when the Trader agreed to buy the cargo from the Explorer with a deemed B/L date of 6th March and 2-1-2 pricing, the Dated Brent component of the cargo was worth $83.79/bbl at that moment in time, and only at that moment in time.

Had the parties agreed alternatively on 13th February, to deem the B/L date to be, say, 4th March with 2-1-2 pricing its value would have been $84.08/bbl. A deemed B/L date of 4th March and 5 after B/L pricing would give a cargo value of $83.67. Or, March whole month average (“WMA”) pricing for any March B/L date would give a cargo value on 13th February of $83.12/bbl.

So, as described in our blog, “Spoiled for Choice”, the default option in the oil purchase contract price formula is 2-1-2 pricing (the option market price) because that is what the cargo seller, the Explorer, prefers. The cargo buyer, the Trader, may want the option to choose 5 days after B/L pricing (the option strike price). That option has intrinsic value on 13th February. The deemed B/L date of 6th March was worth $83.79/bbl based on 2-1-2 pricing. But, on 13th February, the average of 5 days after deemed B/L of 6th March pricing was worth $83.42/bbl (i.e., 2/5 of week 4 and 3/5 of week 5). So, on 13th February, the option to change the pricing basis from 2-1-2 to 5 after B/L, had $0.37/bbl of intrinsic value. It can be said to be 37 cents/bbl in-the-money.

This might suggest that, if the Explorer is aware at all of the forward oil price curve on 13th February, it could seek an increase in the size of G1 by $0.37/bbl to account for the option’s intrinsic value. That is not going to happen. If the Trader is going to have to pay up to a $0.37/bbl higher grade differential, G1, for the option to choose between 2-1-2 and 5 after B/L pricing, the Trader might as well just trade the value of the difference between the two price averaging periods in the CFD market. This is a more liquid and more flexible way of trading the value of the time differential, T, than building optionality into a physical oil contract price formula.

The forward oil price curve will give a different range of opportunities each day from 13th February up until the last day agreed between the Explorer and the Trader for the Trader to exercise its option to deem a different B/L date or a different price averaging period from the default price averaging period in the physical contract. The height and slope of the forward oil price curve are in constant motion and will offer different values for the absolute price, A, and the time differential, T, each day. If the market is volatile, the range of possible prices is likely to be measured in dollars rather than cents, as we illustrated in Table One in our blog “Spoiled for Choice”.

But as we said in this previous blog, hindsight is no guide to the future.

On 13th February the Trader may ask the Explorer for the option to choose the deemed B/L date or the price averaging period by, say, 1st March. It may ask for the right to opt for:

- 2-1-2 pricing, the default option in the contract; or,

- 5 after B/L pricing; or,

- 10 after B/L pricing;

- WMA pricing.

It will be recalled from the previous blog that the option premium is made up, not just of its intrinsic value, calculated as $0.37/bbl above, but of the time remaining until expiry, historic volatility, interest rates and implied volatility.

It is no simple matter to work out scientifically at what premium these so called “spread options” could have been traded in the market on 13th February. It is certainly beyond the mathematical skill of the writer of this blog. Some form of Monte Carlo simulation is probably possible, but one of the problems is that there is no liquid market in non-standard options derived from a physical cargo contract. So, it is hard to get a fix on implied volatility. Hedging the price risk would be difficult, labour-intensive and costly.

In theory, if the Trader could agree a smaller increase in the size of G1 in its physical purchase oil price formula to acquire the option from the Explorer than the premium at which it can sell the option in the market to a third party, it could decide to sell the option. This is unlikely because there is no liquid market in these highly tailored options.

Furthermore, if the cargo purchased by the Trader from the Explorer is part of an arbitrage strategy, such as in the onward sale to the Refiner example above, the deemed B/L and price averaging period are very likely to be hedged, as described above. If that arbitrage depends on the size of G2 in its physical sales oil price formula with the Refiner being sufficiently bigger than G1 in its physical purchase oil price formula with the Explorer to cover its costs, then selling the option to choose the purchase price averaging period to a third party makes little sense. Apart from anything else it would leave the Trader with a difficulty in deciding which price averaging period to hedge in its contract purchase price formula from the Explorer: the choice would be out of the Traders’ hands and determined by the third party to whom the Trader had sold the option.

Hence, deciding how much a small non-trading firm should charge a larger oil company or trader for the right to deem the B/L date or choose the price averaging period is not as simple as discovering the market value of the option on the day the deal is struck. However, the price negotiation will be less one-sided if the option grantor has established an appreciation of the practical shortcomings of any attempt to establish the theoretical option value at the outset.

Clearly, bestowing such an option has a positive value, and as described in our last blog, the more volatile the market and the longer the larger trading company is given to exercise the option, the more favourable should be the option premium to the option grantor.

As we said in our second blog, under the heading “Look Back in Anger”, granting a “look back” option is akin to letting your counterparty call heads or tails after the coin has landed. This will never work in the option grantor’s favour, so the grantor should be seeking a much, much higher premium if it sells this right.

The option premium that the option grantor actually achieves depends mainly on how much muscle it can bring to bear in the negotiation. Trading is an art, not a science.

As we said in our first blog, the only way to ensure that small producers or refiners are getting the best price for their shareholders is for them to award a tender, always to a reliable company from as wide a range of counterparties as possible, that gives the most favourable differential to the tender price formula that is identical in every other respect. If one responder is seeking an option in the deemed B/L date or price averaging period and the others are not, the differentials are not comparable.

If there is only one company, or very few companies, interested in the physical contract, then the scientific valuation of the pricing option is a moot point. There is no point in demanding a higher premium if your need to sell is imperative and there is only one buyer in town. In the words of Dirty Harry: “...you've got to ask yourself one question: Do I feel lucky?' Well, do you, punk?"

The biggest difference between trading and gambling? In trading, the house doesn’t always win. Liz Bossley

Liz Bossley, with thanks to David Povey and Ben Holt for their help in peer reviewing this blog.