6 Fern House

10 Pinewood Place

Windsor SL4 3SP UK

0

£0.00

0 items

The price of oil has always been as much about logistics as it is about oil supply and demand. We have had a few salutary reminders of this fact in recent weeks. There are two pipelines that are attracting particular attention at the moment:

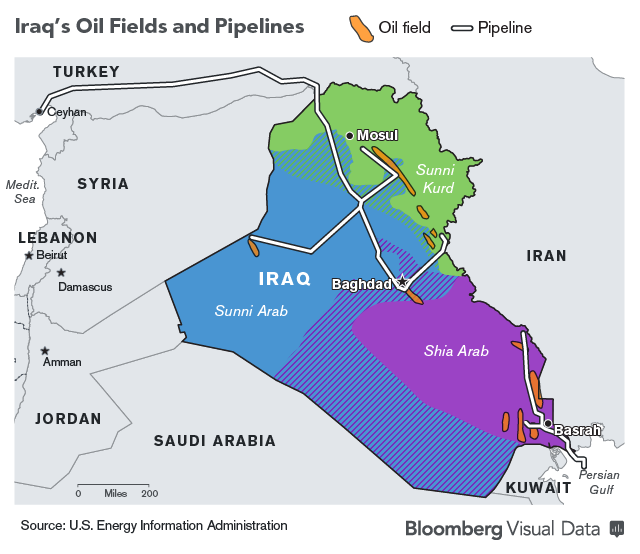

The Kurdistan Regional Government (KRG) is now in control of the oil fields in North Iraq which are gathered at Kirkuk. KRG is exporting oil through Turkey to the port of Ceyhan in the Mediterranean. Although this pipeline has a much larger capacity, exports from Northern Iraq are down to levels of 100-120,000 b/d following the years first of sanctions and then of attacks.

The Turkish government continues to accommodate Kurdish exports in the face of political condemnation. The market waits with bated breath for the other shoe to fall and for the backlash against Kurdish exports to manifest itself. Sadly, this is likely to involve more shooting.

Stopping Kurdish exports by blockade of Ceyhan would not be easy. Any interference with exports from Ceyhan would have a much wider impact than the comparatively small volumes in the Kirkuk- Ceyhan pipeline would suggest. Ceyhan is an important hub in the Mediterranean and for the wider market because it is the outlet for exports from Azerbaijan, Kazakhstan, and Turkmenistan through the Baku –Tbilisi- Ceyhan pipeline, which has a capacity of 1.2 million b/d. (For Kazakhstan and Turkmenistan, entry to the BTC pipeline is achieved by crossing the Caspian by small tanker to the port of Baku.)

Source: Asian Times

This is not a cheap export route, but the alternative , if Ceyhan were to close, is to reach the international market via Russia through the Tengiz to Novorossiysk CPC pipeline, or the direct Baku to Novorossiysk pipeline. Oil at Novorossiysk then faces another journey across the Black Sea and through the Bosphorus/Istanbul bottleneck before reaching the international market in the Mediterranean. Ships can be delayed in transiting the Bosphorus by more than 15 days.

Source: Argus Media

Azeri oil can also reach the Black Sea via the problematic Baku-Supsa pipeline, which has a capacity of ~150,000 b/d. This pipeline has been subject to prolonged shutdowns in the past for maintenance and in response to armed conflict along its route. From Supsa this oil also must transit the Black Sea and the Bosphorous.

A third pipeline from Samsun in the Black Sea to Ceyhan has been delayed by various political disputes, the latest of which is with relates to Turkish refusal to let the pipeline be built by companies also operating in Cyprus.

A blockade to halt Kurdish Iraqi exports via Ceyhan would therefore also disrupt the much larger volume of exports via Azerbaijan, Kazakhstan, and Turkmenistan via the BTC pipeline. Any attempt to apply economic sanctions to only Kurdish exports via Ceyhan would be very difficult to enforce.

Applying economic sanctions against Kurdish exports would provide an inevitable temptation for trading companies to buy Kurdish oil at Ceyhan and to misrepresent it as Azerbaijan, Kazakhstan, and Turkmenistan oil in their onward sales. It is likely that trading companies attempting this sleight of hand would make onward sales on a Delivered Ex-Ship (DES) basis where the end-buyer does not take custody of the oil until it discharges at its refinery. In DES sales bills of lading (B/Ls) are often not available.

Buyers taking crude oil originating from Ceyhan would be well advised to examine their certificates of Quality, Quantity and Origin and the B/Ls carefully, or absent these documents, to ensure that the trader’s letter of indemnity is issued by a first class bank.

For the KRG there will be difficulties in receiving payment for oil, the ownership of which is under dispute. Typically when selling to trading companies, whose financial standing is not verified by a publicly available Annual Report and Statement of Accounts, seller’s will demand that the trader secures payment with a letter of credit (L/C) from a first class bank. But such banks are unlikely to agree to open an L/C for oil the ownership of which is known to be in dispute.

This is a complex situation and there will be further developments.

On 17th June Enbridge received Canadian Federal government approval to build the Northern Gateway pipeline headed west from Alberta through British Columbia to the lucrative Far East market in the Pacific.

Source: Enbridge http://www.gatewayfacts.ca/about-the-project/project-overview/#route-map

This is the pipeline which, it was said, would never be built because of strong environmental opposition, including from the Canadian first nations. There is a lot that could happen to prevent the new export route being completed: Enbridge have to satisfy more than 200 conditions before final approval is granted and the law suits have already started to stop progress.

Canada needs this export route. In 2013 60% of Canada’s exports went to the USA where it fell foul of competition from burgeoning US domestic oil production and the prohibition on the export of USA crude oil. Some Canadian domestic oil is finding its way out into the international market through the US gulf coast because the US ban on crude exports does not apply to Canadian oil.

But this leaves a fair proportion stuck in the US where prices are a good $5-10/bbl below the international market. That discount has been as high as $25-30/bbl. That is very helpful to the US economy, but the Canadian producer and taxpayer is losing out.

Enbridge’s breakthrough in the approval process probably has nothing to do with the build-up of Chinese interests in Canadian oil production, notably through the purchase of Nexen. But it makes you wonder, doesn’t it?