Liz Bossley CEO In The Press…

Your Expert Witness Magazine issue 59

https://www.yourexpertwitness.co.uk/archive-issues/1294

The article on page 19 authored by Liz Bossley

https://www.yourexpertwitness.co.uk/archive-issues/1294

The article on page 19 authored by Liz Bossley

The Brent benchmark is long overdue to be put out of its misery humanely. This tired old workhorse has been limping along with the increasingly onerous burden of being the key reference point for setting the price of, arguably, two thirds to three quarters of the world’s crude oil since 1981: that was when the first 15-day Brent contracts were traded. But, rather than put this beast of burden out to pasture, the oil industry is on the point of choosing to keep it in service with an injection of steroids- the inclusion of West Texas Intermediate (WTI) into the basket of grades of North Sea that form the Brent price currently.

As production has declined over the years, “Brent” has been rejuvenated on several occasions with the introduction of a basket of different grades – Forties, Oseberg, Ekofisk and Troll- that can be delivered into the Brent forward contract, 30-Day BFOET[1], and the Dated Brent price assessment, published by the Price Reporting Agency (PRA), S&P Global Platts.

The disparate quality of these grades has led to the introduction of various quality adjustment factors and a de-escalator in an attempt to bring the value of these different grades into line with the price at which “pure” Brent Blend would be trading, if there was sufficient Brent Blend around to provide a database of actual trades, which there is not. These quality-related factors are:

Then in November 2019, a Rubicon was crossed when trades in these same grades that are sold on a delivered CIF Rotterdam basis were included in the basket, specifically in the formation of the key Dated Brent assessment. Dated Brent refers to cargoes loaded on a rolling 10-30 days forward from each Platts publication date. The CIF prices are netted back to give an FOB equivalent price adjusting for freight, sailing time and port dues. Sailing time and port dues are relatively transparent, but the assessment of freight is a different matter. The amount of freight that is deducted from the CIF price is weighted “by a freight adjustment factor, to account for any differences in optionality between a

[1] Market short-hand has stopped adding new letters to the BFOE acronym, despite the inclusion of Troll. This is something of a relief as further grades are likely to be added to the basket and the possibility of unfortunate anagrams increases.

FOB and a CIF offer”, according to Platts. The cost of freight to which this factor is applied to the 10-day rolling freight average of the Dirty Cross-UK/Continent 80,000 mt freight assessment (you’ve guessed it) as assessed and published by Platts.

The concept of including CIF cargoes in an FOB basket has opened the door for including grades from other parts of the world delivered to Rotterdam. This brings us to the current proposal to include US West Texas Intermediate Midland (WTIM) into the Platts Dated Brent assessment.

WTI used to be well understood as the domestic American grade that was delivered inland to Cushing, Oklahoma and which could be delivered into the CME (NYMEX) futures contract to settle contracts with physical delivery rather than by reference to a cash-settled book-out price. That all changed at the end of 2015 when the ban on US crude exports, which had been in place since 1975, was lifted.

Source: BP Statistical Review 2020

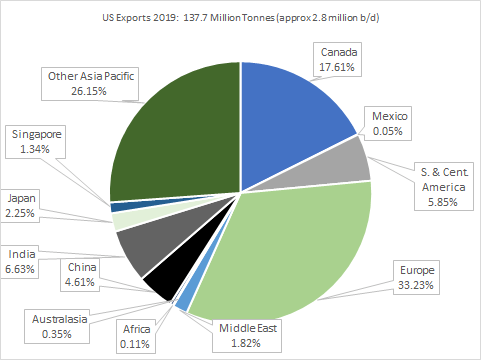

The US exported about 1 million b/d of crude oil to Europe in 2019, and it is this volume that is being considered to boost the database of transactions that may be able to shore up the Brent price benchmark.

Source: BP Statistical Review 2020

Platts is now proposing that the Platts WTI Midland (WTIM) price quotations be included in the assessment of the Dated Brent benchmark from March 2022- a long lead time to allow traders to adjust their contractual arrangements to reflect the new Dated Brent price assessment.

Exploration and production companies, who employ the Dated Brent price assessment in longer term sales contracts, are unlikely to appreciate that this will have an impact on the value of the benchmark price on which their contracts are based. They are equally unlikely to avail themselves of any price re-opener clauses that will allow them to review any price differential between the price of their own specific grade of oil and the new-style Dated Brent.

Among the myriad of other questions that the inclusion of WTI in the Brent basket raises is why use the WTI Midland price quotation? Midland Texas is ~425+ miles from the Gulf Coast from whence exports actually take place. Any price based on Midland Texas is subject to a further variable, namely the cost of transporting the WTI from Midland to Houston. This too would have to be factored out to make WTI trades comparable with Brent FOB Sullom Voe.

WTIM describes crude originating in the Permian Basin, which goes straight down one of the direct pipelines for loading at Corpus or Houston without commingling. This avoids any risk of blending taking place to downgrade the quality, as is suspected of crude arriving from Cushing. Platts places limits on the quality of oil it will accept in its WTIM assessment, although it has no power to change the actual quality of the crude that is shipped.

An alternative WTI quotation that is liquid and closer to the coast, but not actually on the coast, is WTI at Magellan East Houston (WTI MEH). This grade trades at a premium to WTIM and is mainly supplied into US Gulf Coast refineries because of its convenient proximity. Exports of WTI MEH require transportation between US ports, an activity that remains subject to the Jones Act. This Act obliges all shipments between US ports to be conducted on US-flagged, US-built, and US-crewed vessels. This bumps up the costs above international freight rates. So, while WTIM delivered at place (DAP) Rotterdam is an active market, WTI MEH is not. WTIM looks likely to win out in any discussion of including WTI in the Brent basket.

The nature of the WTIM trades that Platts proposes to include in the Dated Brent assessment are not only WTI Midland DAP Rotterdam, but will include any WTIM oil trans-shipped and sold FOB Scapa Flow in the Orkneys Isles off the North Coast of Scotland. In reality, little, if any WTIM, has ever traded on an FOB Scapa Flow basis. Rather, it is proposed that deals done DAP Rotterdam are to be netted back to an FOB Scapa flow basis by Platts before inclusion in the Dated Brent price database. Hence, the cost of bringing WTIM to Scapa flow would not necessarily be a feature of the price assessment of WTIM in the Brent basket.

It may be argued that the origin of the WTI that arrives at Rotterdam is irrelevant, other than for establishing the quality of the WTI that is being proposed for inclusion in the Brent basket: what is called WTI varies in quality depending on the pipeline system used to gather it[1]. Precisely how any quality adjustment that will be needed to fit WTIM into Brent basket quality will be done is still up

[1] WTI Midland API 38-44o, sulphur <0.45%; WTI MEH API 42 o, sulphur 0.15%; WTI Cushing API 41 o, sulphur 0.4%, according to Platts.

for discussion in Platts’ consultation which ends on February 5th 2021. But it increases the significance of Ship-to-Ship (STS) transfers in Scapa flow in the Dated Brent price assessment process.

WTIM in Brent is another step along the path of including a range of grades from further afield into the Dated Brent assessment process.

The amount of deal evidence, or rather the lack of it, is the whole crux of the problem. The burden of Brent rests on deals, or more often, just bids and offers, posted in the Platts window by a restricted number of traders during a half hour period. A lot of this database is made up of part cargoes, not full cargoes. The responsibility for filling in any blanks has been relinquished by the oil industry to Platts.

This may suit the industry quite well. It relieves the oil companies and trading houses of a lot of the effort needed to have a say in the price that will show up in physical contracts all around the world. The existence of the Platts window concentrates the focus of price discovery for contractual purposes into a short half hour period and a small volume of trade each day.

Theoretically, the industry could get together and convene an independent panel to take the methodology for establishing benchmark pricing back into the hands of those that are active in the market. But the spectre of anti-trust regulations provides a convincing get-out clause for pursuing any such idea.

Ultimately, the oil trading community has got the oil price formation process for which it has been prepared to settle and which, perhaps, it deserves.

She has at the same time joined the editorial board of the AIPN’s quarterly Journal of World Energy Law and Business.

Regular readers of Liz Out Loud, who we hope will opt in to continue receiving our emails following the implementation of GDPR, will be very aware that there is considerable dissatisfaction with the current basket of very different grades of oil that underlies the Dated Brent price benchmark and the 30 - Day Brent/ Forties/ Oseberg/ Ekofisk/ Troll (BFOET) forward Brent market.

This blog makes a practical suggestion for how the mechanics of the quality issues currently facing the Brent basket might begin to be addressed and invites readers to contribute their own suggested refinements, improvements or alternatives anonymously.

Background

The volume of oil in the Brent basket is declining and it is becoming increasingly apparent that new grades will have to be added to prevent any attempts to corner the market and to provide enough deal evidence to justify the prices reported by Price Reporting Agencies (PRAs).

One of the biggest stumbling blocks to adding new grades to the basket successfully is the increasingly disparate quality of the basket grades, currently Brent, Forties, Oseberg, Ekofisk and Troll. The current system of Quality Premia for Oseberg and Ekofisk and the sulphur price de-escalator applied to Forties is not adequate to the needs of the assessors of the Dated Brent price benchmark, the PRAs, or to the 30-Day forward market. Buyers of forward Brent can receive any one of the current five basket grades of oil which are becoming increasingly disparate in quality.

Hopes of including Johann Sverdrup in the basket when it comes onstream late in 2019 depend upon the goodwill of the operator, Equinor, the company formerly known as Statoil, in ensuring that cargo sizes and the scheduling of liftings is compatible with the other 5 grades in the existing basket. But equally important is the need for the industry to reach consensus on how best to continue to enhance the volume of oil in the basket by bringing in more and different grades into it by introducing a mechanism for compensating buyers when they buy “Brent” but receive an entirely different grade with different quality attributes.

How a GPW-based Price Differential could work in practice

One of the ideas currently under consideration is the use of a Gross Product Worth (GPW) calculation to establish a market price differential amongst all the grades in a basket.

A GPW is calculated as follows:

GPW ($/bbl)= Σ[ ((Mt of Product 1) x (Price per Mt of Product 1) x (Mt to bbls conversion factor for Product 1)) + ((Mt of Product 2) x (Price per Mt of Product 2) x (Mt to bbls conversion factor for Product 2)) + ((Mt of Product 3) x (Price per Mt of Product 3) x (Mt to bbls conversion factor for Product 3))…………..etc. ]

In other words if you take the quantity in tonnes of each product that can be extracted from a barrel of oil and multiply each product by its price per tonne, convert each product value from tonnes to barrels using the appropriate conversion factor for refined products of that API gravity and add the result up for all the refined products in the barrel, you get an idea of the value to a refiner of a barrel of the grade of oil in question.

Critics of this methodology are quick to point out that the GPW of a barrel of oil is not synonymous with its market price. The market price is influenced by factors other than quality and may be quite different from the GPW that any individual refinery can extract from it. Those refineries that can extract more in GPW than the market price will compete to buy and refine that grade. Those refineries that cannot extract more GPW value than the market price will look for other grades to buy. Nevertheless the GPW can be handy proxy for establishing the market price differentials amongst different grades of oil in a basket if the GPW calculation parameters are chosen with care.

One of the first decisions to be taken in calculating a GPW is which refinery should be chosen to calculate the quantity of each product yielded by each grade? The answer will be very different if a primary distillation “tea kettle” is used rather than a sophisticated coker that squeezes every last cent of value out of a barrel of crude oil.

It may be said that the refining of grades in the BFOET basket occurs predominantly, although not exclusively, in the N.W.E. catchment area. So it would, in my opinion, be appropriate to calculate the GPWs of basket grades in the type of refineries that operate in that area.

An actual existing N.W.E. reference refinery need not be selected. But one could be constructed artificially by averaging the Nelson complexity indices of all the refineries active in the relevant area.

Nelson Complexity Index

The complexity factors (CFs) of refinery processing units are published annually by the Oil and Gas Journal, allowing the Nelson Complexity Index (NCI) of any refinery, or group of refineries, to be calculated and updated whenever a refinery is upgraded or when any of its units are closed down. Primary distillation capacity is given a CF of 1 and each secondary processing unit is assigned a CF according to the amount of investment it requires and the value it adds to a barrel of oil.

For example an FCC unit might have a complexity factor of 6 where as a very expensive and high value added lube unit might have a complexity factor of 60. The NCI is calculated by summing the complexity factors (CFs) of each unit in the refinery multiplied by the capacity of each unit relative to primary distillation capacity.

NCI = Σ [(CFdistillation x Distillation capacity/ Distillation capacity) + (CFUnit 1 x Unit 1 capacity/ Distillation capacity) + (CFUnit 2 x Unit 2 capacity/ Distillation capacity) + (CFUnit 3 x Unit 3 capacity/ Distillation capacity)….etc.]

So a European Reference Refinery could be constructed with an NCI equivalent to the weighted average of all European refineries. It would then be possible to calculate the GPWs of all the grades in the existing or future Brent basket using this Reference Refinery. This may be done using neutral, off-the-shelf refinery modelling software such as that sold by Haverly Systems (1).

As stated above, the GPW of any crude rarely coincides with its market price. But the purpose of this exercise is not to establish the absolute value of the grades of oil in the Brent basket, only their values relative to each other, i.e. the price differentials. To test the robustness of the methodology the components of the NCI of the Reference Refinery can be tweaked to find the closest fit to, or correlation with, actual historic market price differentials amongst the basket grades.

Which Product Prices?

Initially it may be wise to use Amsterdam Rotterdam Antwerp (ARA) product prices when calculating relative GPWs, while the majority of the volume of oil within the Brent basket are still refined in N.W.E. But over time if grades from outside N.W.E. were to be added to the basket then there may be a need to introduce weighted average product prices and additional refineries from outside the catchment area.

These product prices would be updated daily as the PRAs update their data so that the crude oil price differentials generated reflect daily assessments of the future crude oil price differential based on product prices that apply to refined products being delivered up to 25 days in the future. One way of implementing this methodology would be to apply the GPW differential generated by the modelled published on the day on which a cargo is declared into a 30-Day BFOET chain.

So 30 days before the first day of the loading date range of a given BFOET cargo, the seller would declare to the buyer the date range and the grade it will deliver into its 30 Day BFOET(JS?) contract. The price differential that would apply if the cargo is not Brent, which it rarely is, but is Forties, Oseberg, Ekofisk, Troll (or Johnann Sverdrup?), would be the GPW differential published by the PRAs at close of business on that same declaration day.

It is to be anticipated that any GPW-based method of calculating price differentials will require maintenance to ensure that the Reference Refinery is up-to-date with the addition of new processing units or refinery closures either for maintenance or permanently. If the differential calculation methodology began to diverge from actual market price differentials then this would indicate that the NCIs or the RR or the product price set required adjustment and that a tug on the kite strings was needed.

Otherwise it would be a simple case of cranking the handle on the differential machine daily to churn out the quality adjustment factor, i.e. the GPW differential, that has to be applied when a basket grade of crude oil other than Brent is delivered into a 30-Day BFOET+ contract.

The objective of this somewhat cumbersome exercise is to improve liquidity in the 30-Day forward Brent market that underpins the regulated Brent futures and OTC swaps and options markets.

Views on the quality issue and this suggested methodology for establishing price differentials are very welcome and can be submitted anonymously below.