6 Fern House

10 Pinewood Place

Windsor SL4 3SP UK

0

£0.00

0 items

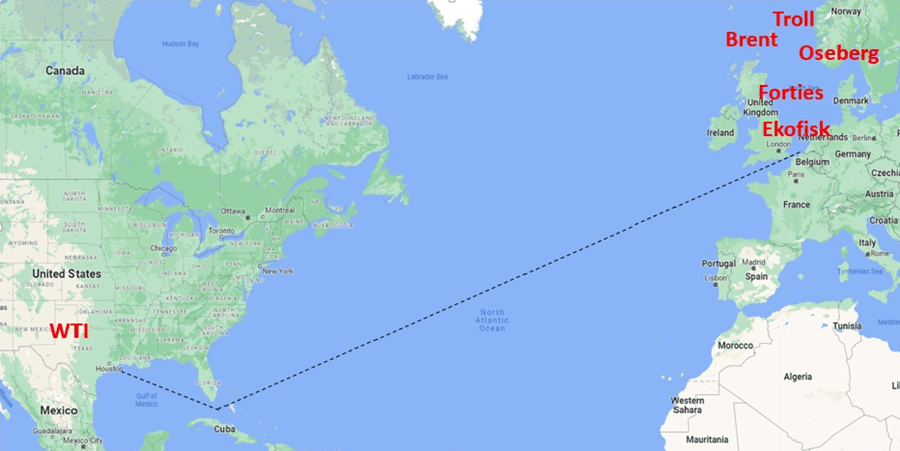

...it is evident that what is now called Brent is a completely different animal from what we called Brent back in 1983, when 15-Day Brent started trading. Brent is now an artificially constructed price index based on a small number of deals, sometimes no deals at all, only bids and offers that do not necessarily result in a contract. These data points are provided by a limited pre-approved number of counterparties over a very brief period of time, a dealing “window”, each day.

Interested parties, oil companies, trading companies, price reporting agencies (“PRAs”) , exchanges, and banks have bent over backwards to keep the brand name “Brent” going long after production from the Brent oilfield dwindled to a trickle. To shore up the volume of production that can lead to reportable transactions that can inform the price assessment process, increasingly disparate grades of crude oil have been added to the basket that constitutes Brent over the years. This has necessitated the inclusion of sulphur price de-escalators and quality-related price adjustments to appease those who buy or sell Brent, but end up with delivery of Forties, Oseberg, Ekofisk or Troll instead. The inclusion of new grades in the basket has proved to be not enough historically to maintain liquidity in the Brent contract. So, datapoints emanating from transactions done CIF Rotterdam were introduced to be netted back to an FOB North Sea basis to further pad the information available to the PRAs when they construct their assessments. That was still not enough.

WTI Midland into Brent

So, from June 2023 it is intended that WTI Midland, Brent’s most credible rival for international benchmark status, will be annexed into the Brent basket. To appropriate WTI into Brent, a substantial upheaval in trading custom and practice is underway. Not only is WTI of different quality from the existing components of the Brent basket, it is located on the opposite side of the Atlantic and tends to get transported in tankers of a different size than those in common use in North West Europe. Upstream producers in the North Sea are, de facto, being asked to cooperate with an increase in cargo sizes in the upstream lifting agreements to 700,000 bbls to make them compatible with US exported WTI. This is being achieved by extending the loading time allowed for vessels to accommodate larger cargoes. There is no reason why minority partners in fields that load through the Brent basket terminals should go along with this change: for small producers the increased cargo size delays their accrual of a full cargo, which has significant pricing and cash flow implications. Small producers can still load smaller cargoes if they want to. However, if the rest of the market wants cargoes of 700,000 bbls, good luck with trying to get top dollar for a 600,000 bbls cargo. The scheduling of WTI cargoes takes place in accordance with a US domestic pipeline timetable, not a North Sea monthly lifting schedule. But to preserve the Brent brand name, US Gulf Coast terminals are changing their timetables for nominating the lifting cargoes of WTI and limiting the range of pipeline qualities they accept to allow them to sell WTI into the Brent complex via delivery CIF Rotterdam.

Who Is the Regulator?

The point where risk and title to the oil passes from WTI sellers to buyers is being changed to just outside the US economic exclusion zone, rather than FOB the loading point, which is the actual , or netted back delivery point in Brent basket contracts. This is reputedly to keep those cargoes of WTI going into Brent, and arguably Brent itself, out of US jurisdiction and the US tax net. Whether this device will be effective remains to be seen. Those readers who were trading in the late 1980s and early 1990s will recall the ruling by Judge William Connor that Brent trades constituted a futures market under the U.S. Commodity Exchange Act and came under the jurisdiction of the Commodity Futures Trading Commission (“CFTC”). This alarming statement prompted furious back-peddling by the CFTC and out-of-court settlements by the protagonists in the case. If the status of Brent with WTI included ever gets challenged in a court, it is anyone’s guess what the outcome and consequences would be.

Who Needs Who?

The WTI Midland market has legs of its own and does not need Brent. In fact, one PRA stated in an International Energy Week presentation that WTI is not joining Brent, but that Brent is being swallowed by WTI. Waning Brent needs the burgeoning volume of activity associated with WTI Midland to survive. It would be considerably simpler to let Brent atrophy and for WTI and/or some other benchmark to take over by a process of evolution. But those parties with a vested interest are going to extraordinary lengths to keep Brent alive.

ISDA and the Material Change Question

One possible reason is the “Material Change in Formula” provisions of the International Swaps and Derivatives Association (“ISDA”) master agreements that are entered into by over-the-counter swaps and options traders. These sit behind long-term positions entered into for the strategic hedging of oil field developments and for the loan financing of those developments. A Material Change in Formula means the occurrence since the date of the deal in question of a material change in the formula for, or the method of, calculating the contract reference price. This may constitute a “disruption event”, in ISDA terminology, and a “calculation agent determination” of an adjustment to the price to bring it back into line with the original intention of the contract. It may even constitute a “termination event”, in other words the end of the contract. This takes us into some murky legal waters outside this writer’s area of expertise.

Arguably, there have been several material changes in Brent over the years, but none quite so material in my opinion, as the inclusion of WTI into the Brent basket. So far, the fact that the benchmark has kept the brand name “Brent”, may have protected it from challenge by the occasional disgruntled contract holder sitting on a loss-making position. Traders with nothing left to lose just might be tempted to have a go in court at claiming that a deal they entered into some time ago did not envisage such a significant change to the benchmark price. Any update to the brand name following the inclusion of WTI, such as calling it “the Atlantic Basin Benchmark”, or something similar, would increase the risk of triggering claims of “Material Change” re-openers under ISDA contracts, whether justified or not.

Changing Price Differentials

The PRAs are changing their Brent price assessment process after consultation with industry, although the new methodology is not universally popular with all the major industry players. Many industry participants that use Brent as a benchmark in contracts are actually oblivious to the workings of the Brent market. They may not appreciate the fact that WTI is likely to be the most competitive grade in the Brent basket most of the time, i.e. the cheapest grade in the basket, for prolonged periods of time. WTI tends to trade at a discount to Brent. This means that the Dated Brent price in those periods will be lower than it otherwise would have been if WTI was not in the basket. This has implications for the grade differential in contracts. If the benchmark price is lowered by the inclusion of WTI, the grade differential has to be adjusted upwards to compensate for this fact. It is debatable how quickly small companies without active trading departments, national oil companies that use Dated Brent as a benchmark, or revenue authorities that use Dated Brent as their tax reference price in upstream agreements, will be cotton on to the implications of the changing composition of Brent.

“With great power comes great responsibility.”

The band aids necessary to keep the Brent brand name in common use, despite some substantial changes to the composition of the Brent basket, such as sulphur de-escalators, quality premia, freight adjustment factors etc., are not negotiated and announced by industry participants. They are assessed and announced by PRAs, albeit by observing such trades as are disclosed to them and by having discussions with some eligible market participants. No-one is forcing oil industry participants to adopt methodologies or price assessments determined by a PRA, or to use the price of Dated Brent or cash Brent as a price benchmark in their contracts. Nor are they forced to adopt the general terms and conditions of trade published by major oil companies. But for any one company to hold out against the custom and practice in common use by the dominant players in the market would be to swim against the tide.

https://ceag.org/shop/web-apps/oil-field-production-and-revenue-raah-monthly-payments/

RAAH is an easy-to-use analytical tool designed to help crude oil producers and oil asset buyers and sellers to evaluate their producing and developing oil field projects based on varying production forecasts, different price assumptions and in a wide range of royalty, cost recovery, profit sharing and tax regimes.

RAAH is not based on any one specific country’s petroleum legislation, but includes the components of the production sharing contracts that are encountered repeatedly around the world- royalty paid in cash or in-kind, cost recovery, profit sharing with the government or NOC, petroleum tax and corporation/profit tax.

This software allows the user to tailor the analysis to its own situation by inputting appropriate assumptions for each project. This encourages the user to focus on the assumptions it is making about the project and highlights the consequences if these assumptions turn out to be wrong.

RAAH provides a template to evaluate up to 20 separate oil field projects over a 20-year period, divided into calendar quarters, based on different:

The Purpose of RAAH

The RAAH software tool is designed to ensure that the revenue assumptions that are plugged into the user’s economic model of a field or project have been thought through thoroughly. It allows the user to play around with a wide range of “What if?” scenarios to make sure it has considered the consequences if its assumptions turn out to be wrong.

RAAH generates almost 500 tables and over 250 charts instantaneously when the user inputs data for up to 20 fields over a 20-year period. It also allows users to import data from Microsoft excel to permit rapid input of large blocks of data and to export the resulting outputs to Microsoft excel to permit the user to incorporate RAAH results into other applications